Everyone seems to be talking about state budgets and governors performance. I guess Menzie started things out with this post. Joe Wiesenthal followed up with this post. Although the job creation performance of Governor Walker in Wisconsin and Governor Kasich in Ohio are not resounding successes they are not complete failures either. In a recent post I found both states showed a dramatic improvement in business environment over the last two years according to ChiefExectutive.net. Unfortunately popularity with chief executives does necessarily translate into jobs. The optimism of chief executives is not echoed in the 2012 State Business Tax Climate Index report by Tax Foundation. Wisconsin is number 43 on the list and Ohio is number 39.

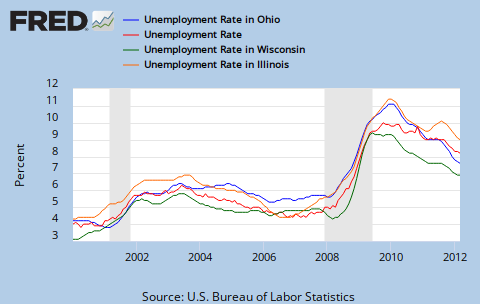

Since Menzie pursued the job creation angle, I decided to use Fredgraph to create an unemployment graph for Wisconsin, Ohio, Illinois, and the United States, http://research.stlouisfed.org/fredgraph.png?g=7eN. Looking at the graph I am not sure I would be complaining too much if I lived in Wisconsin. It could be worse. The job situation is much more precarious in Illinois. Although Menzie correctly points out that the job creation in in Wisconsin is pretty anemic, both Wisconsin and Ohio unemployment rates are below the national average. This is pretty good job performance considering how poorly they rank in business tax climate. Unfortunately most of the future job gains in Wisconsin and Ohio will probably come from job losses in other states such as Illinois. If Illinois’s unemployment rate remains above the average, their government financing remains a mess, and if either Wisconsin or Ohio can improve their business tax climate to a Illinois’s level, then Wisconsin and Ohio should be successful at poaching jobs from Illinois. This should be a major part of any jobs plan along with new jobs created by green industries and shale gas.

{kind=link}